What is Reference-Based Pricing (RBP)?

Reference-Based Pricing (RBP) is a method for determining what a health plan pays a provider, using transparent, objective benchmarks — such as Medicare rates or industry cost data — instead of the provider’s billed charges. By starting with a clear reference point rather than unpredictable pricing, RBP brings fairness and transparency to medical payments.

How RBP Works

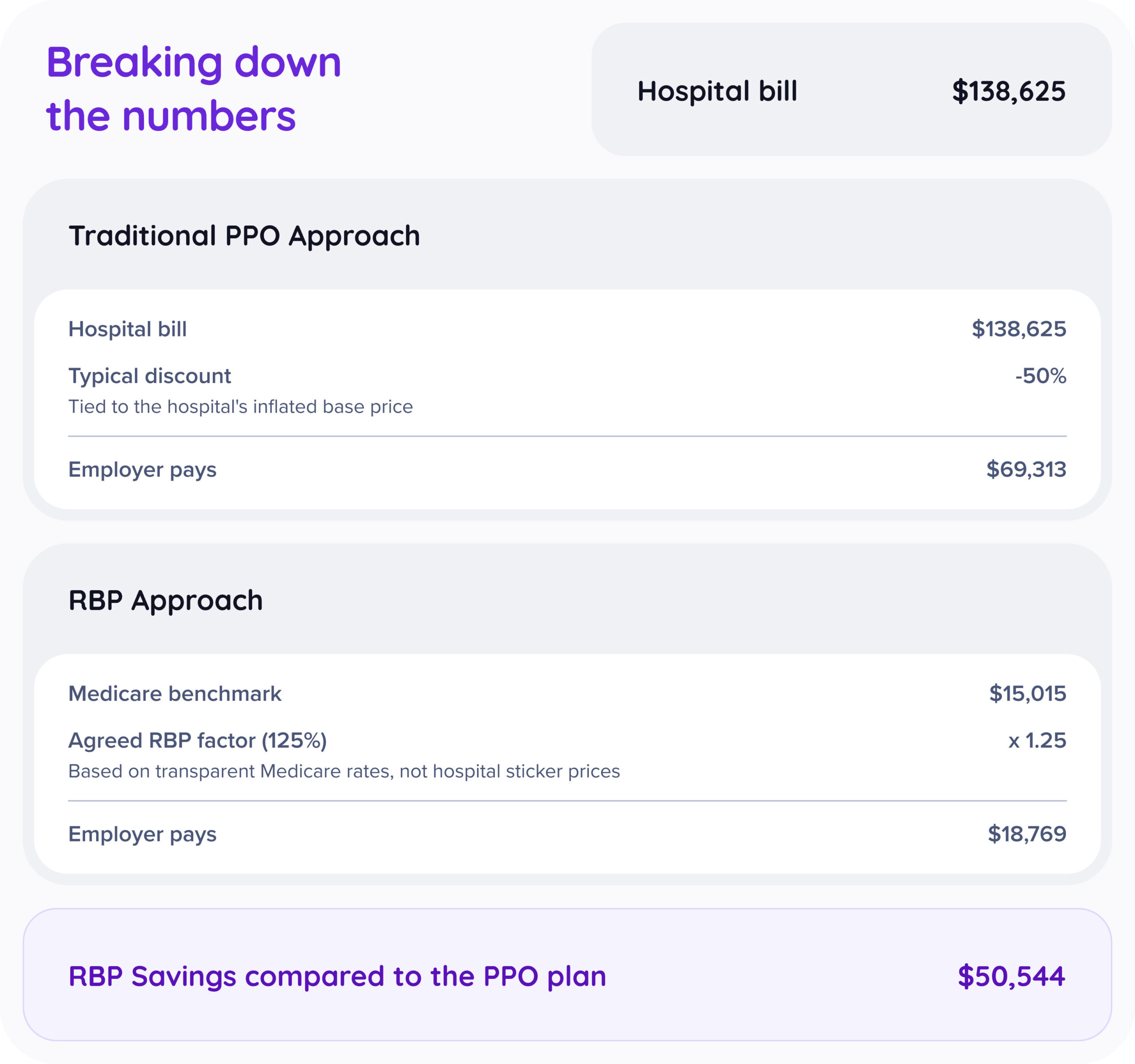

At its core, RBP determines what the health plan will pay a provider by using an objective benchmark rather than billed charges. Each medical bill is compared against this benchmark (most commonly Medicare’s cost data) to determine a fair reimbursement. The benchmark reflects what it truly costs to deliver a service, and the plan pays a percentage above that amount. This percentage can vary by service type, facility, and market norms.

Once payment is issued, the provider can either accept it in full or contact the plan with questions. Strong RBP partners manage these conversations directly with the provider, keeping members out of the middle and ensuring a smooth experience.

- A member sees a provider of their choice.

- The provider sends the bill to the health plan

- The plan reviews the claim and determines payment based on transparent data, such as Medicare rates.

- The plan pays the provider a fair percentage above that benchmark.

- If the provider has questions or requests more payment, the plan communicates with them directly.

- The member is responsible only for their normal cost-sharing (copays, deductibles, coinsurance).

At Homestead, we pair RBP with robust concierge member support, proactive communication, and dedicated advocacy, so no one feels alone or exposed.

How RBP sets reimbursement rates

Because facilities set their own prices, the cost of the same service can vary dramatically. Traditional PPOs start with a provider’s billed charges and apply a discount. RBP reverses the model by paying a fair percentage above a transparent benchmark instead of a discount off inflated charges.

A 2024 JAMA study shows that commercial insurers often pay far more than Medicare, typically around 170% of Medicare for inpatient care and 220% for outpatient care.*

RBP and provider choice

Unlike PPO plans, RBP does not depend on a contracted network of in-network or out-of-network providers. Instead of limiting care to specific hospitals or negotiated contracts, RBP uses a transparent payment methodology that applies consistently across providers. This gives members greater flexibility.

Members can generally visit any provider they choose, as long as that provider is willing to accept the plan’s payment. Many providers are familiar with Medicare-based methodologies, which makes RBP reimbursement easier to understand. With no network to stay “in,” members can choose their providers based on quality, convenience, or personal preference.

What RBP is built to do

- Give employers cost stability

- Support members with compassion and guidance

- Pay providers fairly, using data and defensible benchmarks

- Reduce hidden markups and the “surprise” element from medical billing

- Create a calmer, more predictable care experience for everyone involved

Why do many employers choose RBP?

- Costs become consistent and more predictable

- Members get personalized guidance navigating the system

- Employers gain transparency into what they’re paying for

- Waste, markups, and inflated charges are reduced

- Providers receive fast, fair payment based on defensible data

Where RBP works best

RBP is especially effective for employers who want greater control over their health plan spending, value transparent pricing, and prefer flexibility over traditional network limits. It works particularly well in self-funded and level-funded arrangements, where employers already have visibility into claims and can benefit from long-term, sustainable cost strategies.

Fully insured employers can also transition to RBP, often as part of a move toward self-funding or level-funding. With clear education, strong onboarding, and the right partner support, employers can successfully shift from a traditional network model to a benchmark-based approach to reap the benefits.

Keys to a successful RBP plan

RBP is most effective when backed by a strong partner who provides:

- Comprehensive claim auditing to ensure accurate, defensible payments

- Clear provider communication to avoid confusion and build trust

- Experienced negotiation and advocacy if a provider requests more payment

- Member education and support so employees know what to expect

- Transparent reporting for employers to monitor plan performance

These elements create a smooth experience and help employers realize the full value of RBP.

RBP: Myths vs. Realities

Myth #1

“RBP underpays hospitals.”

Reality

RBP uses transparent, data-driven benchmarks, not arbitrary discounts. These benchmarks are commonly accepted through public programs and help reduce the extreme price variation that exists.

RBP pays hospitals based on data-backed benchmarks, often set as a percentage above Medicare or other objective reference points. Many hospitals publicly accept these amounts through government programs. RBP is designed to bring consistency to pricing. In many markets, the same procedure can vary by several hundred percent from one facility to another. RBP helps reduce that extreme variation by anchoring payments to transparent, defensible methodologies.

Myth #2

“Members will constantly get balance bills.”

Reality

Balance bills can happen with any plan, but they are not automatic or common. When providers understand the methodology and communication is clear, the process is typically smoother and more predictable.

While balance bills can occur under RBP, they are not automatic or guaranteed. A balance bill happens when a provider chooses to ask the patient for the difference between their billed charge and the plan’s allowed amount. Many RBP programs include education, communication, and support to help reduce the likelihood of balance bills and ensure members understand what to expect. When providers are informed early, and payments are based on transparent, data-driven benchmarks, the process is typically smoother and more predictable for everyone involved.

Myth #3

“Hospitals hate RBP.”

Reality

Many hospitals work directly with RBP plans when rates are fair, and communication is consistent. Challenges usually come from long-standing pricing structures – not from the care itself.

Hospitals value predictability and clarity. Many are willing to work directly with RBP plans, especially when reimbursement is fair, communication is clear, and payment is timely. Tension often stems from longstanding hospital pricing strategies and legacy contracting models, not from the clinical care itself. When RBP is supported by relationship building, fair rates, and reliable payment behavior, hospital interactions improve significantly.

Myth #4

“RBP limits where I can go for care.”

Reality

RBP is often open-access. Members can generally choose the doctors and hospitals that work best for them, as long as the provider is willing to accept the plan’s payment.

RBP is often designed to be open access, meaning members are generally free to seek care from a wide range of providers. Rather than relying on a traditional network, the plan uses its reference methodology to determine payment. Members can typically choose the doctors and hospitals that work best for them, as long as the provider is willing to accept the plan’s payment terms.

FAQs

Frequently asked questions

Will my employees still be able to choose their own doctors?

Yes. Most RBP plans offer broad provider choice because they don’t rely on a contracted network. Members can generally see any provider who is willing to accept the plan’s payment.

What happens if a provider doesn’t accept the RBP payment?

If a provider requests more than the plan’s allowed amount, your RBP partner steps in. They communicate with the provider, explain the reimbursement methodology, and work toward a resolution. Members are supported throughout the process and not expected to negotiate on their own.

How often do balance bills actually occur?

Balance bills can happen with any plan, but they are not automatic or common. Strong RBP partners combine proactive provider communication, member education, and skilled advocacy, which significantly reduces the likelihood of balance bills and helps resolve issues quickly when they arise.

Do providers really understand RBP?

Many providers are familiar with Medicare-based methodologies, making RBP easier for them to understand. Clear, timely communication from the RBP partner also helps eliminate confusion and sets accurate expectations for payment.

Is RBP the same as going “out-of-network”?

No. RBP does not use traditional “in-network” or “out-of-network” definitions. Payment is based on a benchmark, not a negotiated contract. As long as the provider accepts the plan, members are not penalized with higher out-of-pocket costs when choosing a provider of their choice, since there are no network restrictions.

What kind of savings can employers expect?

Actual savings vary by employer, location, and utilization patterns. However, studies consistently show that commercial insurers often pay hospitals far more than Medicare – sometimes 170%-220% of Medicare rates. By anchoring payments to transparent benchmarks, many employers see meaningful, sustainable reductions in total healthcare spend.

Is RBP hard for employees to understand?

RBP is new to many people, but with clear communication, simple educational materials, and a strong concierge support team, members quickly learn how it works. The most important thing for employees to know is that they’re supported.

Can fully insured employers move to RBP?

Yes. Many fully insured groups begin exploring RBP because of rising premiums, limited transparency, and the desire for more control over their health plan costs. RBP is often considered part of a transition to self-funding or level-funding. With proper onboarding, member education, and a thoughtful plan design, fully insured employers can successfully shift from a traditional network-based model to an RBP approach and potentially realize meaningful savings in the process.

Does RBP impact the quality of care employees receive?

No. RBP only changes how a claim is priced and paid, not the care itself. Members can still choose any provider willing to accept the plan’s payment, and clinical decisions remain entirely between the patient and their doctor. The goal of RBP is to make the cost of care more transparent and predictable, not limit access or alter treatment.

Is RBP compliant with federal regulations?

Yes. RBP is a widely used and compliant reimbursement methodology when implemented correctly. Payments are based on data-driven benchmarks, and plans are required to follow all applicable regulations, including ERISA and ACA requirements. A strong RBP partner ensures the methodology, communication, and member protections meet all regulatory standards.

Have more questions?

Interested in partnering with us?

Let’s build a smarter, more sustainable health plan together.